Commercial Property Insurance

Commercial property insurance helps protect your building, equipment, and inventory, and Infinite makes it easy to compare top carriers. Share a few details to see options that match your property type and budget.

Partnered with 100+ carriers to help you find the best value.

If you own it, lease it, or store inventory in it, it needs to be covered.

Commercial property insurance covers your physical assets against common losses like fire, theft, vandalism, and certain weather events. It can apply to the building, business personal property, and tenant improvements, depending on how your policy is set up. One uncovered loss can pause revenue, disrupt customers, and force expensive short-term fixes. Infinite helps you spot coverage gaps early, compare what’s actually included, and choose limits and deductibles that fit how you operate.

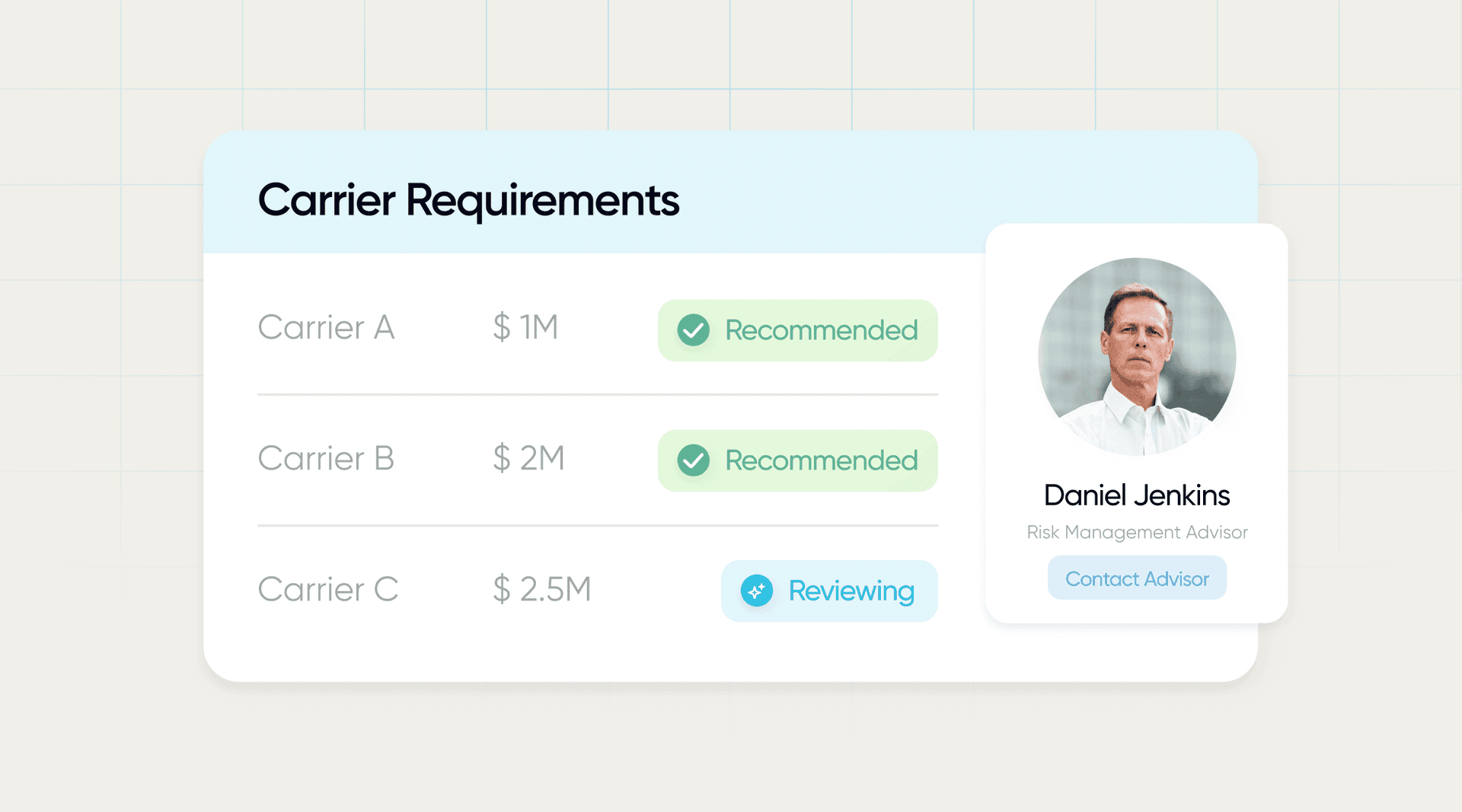

How do you compare commercial property quotes in one place?

Pricing can swing for the same address because carriers rate construction, occupancy, protection (sprinklers, alarms), and loss history differently. The cheapest quote can also come with tighter endorsements, higher wind/hail deductibles, or lower sublimits on key items like signs, glass, or outdoor property.

Infinite brings multiple A-rated markets to the table and puts the details side by side: limits, deductibles, valuation approach, and the endorsements that matter for your building and inventory.

Replacement cost vs. actual cash value matters more than you think.

Commercial property insurance can pay replacement cost or actual cash value, and the difference shows up when you file a claim. Actual cash value factors in depreciation, so older roofs, HVAC, and buildouts may get paid out at a fraction of what it costs to replace today.

Infinite helps you choose the right valuation, avoid surprise depreciation language, and document what you have so your policy is built to rebuild, not just reimburse.

Business interruption coverage can save your company after a loss.

Business interruption coverage helps replace lost income and pay ongoing expenses while a covered property claim is being repaired. It can also include extra expense coverage to keep you operating, like temporary space, expedited shipping, or short-term equipment rentals.

Infinite helps you estimate a realistic limit and time period based on your revenue, payroll, and recovery timeline, so you are not underinsured when downtime hits.

Own multiple locations or lease your space? That changes your coverage.

If you operate at more than one address or lease your space, your policy should clearly match who owns the building, what you own inside it, and where your property moves day to day. Landlord coverage usually stops at the structure, while tenant improvements, inventory, and equipment need to be insured under your policy.

Infinite structures coverage around your real setup, including schedules for multiple locations, blanket limits where appropriate, and endorsements for off-premises property, transit, and storage.

Why businesses choose Infinite for smarter property coverage.

Real reviews on fast comparisons, clear guidance, and support that stays with you after you bind.

QUESTIONS & ANSWERS

FAQ

Have Questions? Talk to Us

By submitting, you agree to our Privacy Policy and Terms of Service.