Business Owners Policy (BOP)

A Business Owners Policy (BOP) bundles general liability and property coverage into one policy, often at a lower cost than buying them separately. Compare top carriers and get a BOP that fits your location, operations, and budget.

Partnered with 100+ carriers to help you find the best value.

Two essential coverages. One policy. Usually cheaper than buying them apart.

A BOP typically combines two core protections: general liability for third-party claims and commercial property for your building or business personal property. For many small and mid-size businesses, it is the simplest way to cover everyday risk without managing multiple renewals. The right choice depends on your industry, revenue, location, and what you actually own or lease.

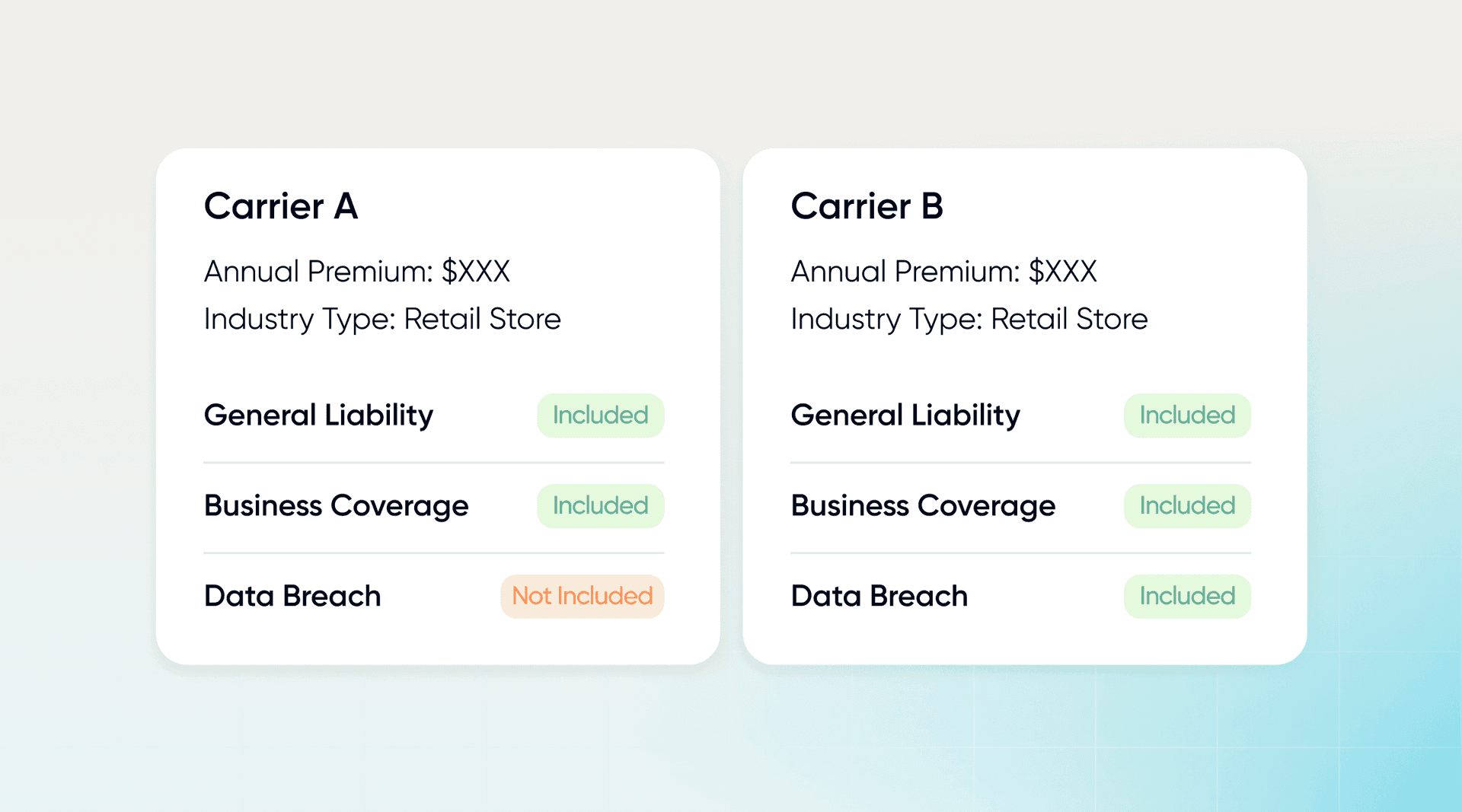

How do you compare BOP quotes in one place?

Business Owners Policy pricing varies by class code, location, revenue, payroll, and square footage, and carriers treat the same business differently. The premium can also change based on property valuation, deductibles, and what endorsements are included.

Infinite shops multiple A-rated markets and shows you the differences side by side, including liability limits, property limits, deductibles, and key inclusions so you can pick the best fit before you commit.

Not every BOP covers the same things.

A Business Owners Policy (BOP) is a package, and the package contents vary. Some BOPs include business interruption by default, while others require an endorsement. Some include equipment breakdown, hired and non-owned auto liability, or cyber add-ons. Others exclude certain operations entirely.

Infinite walks you through what each quote includes, what is excluded, and which add-ons actually matter for your business, so you are not surprised when you file a claim.

When is a BOP not the right move?

If you have complex property exposures, high hazard operations, significant foot traffic, or higher limits that a BOP cannot provide, standalone general liability and property policies may be a better fit. Some industries also fall outside standard BOP eligibility depending on carrier appetite.

Infinite will tell you when a BOP is the right tool and when it is not, then structure the alternative cleanly so you do not pay for coverage that does not match your risk.

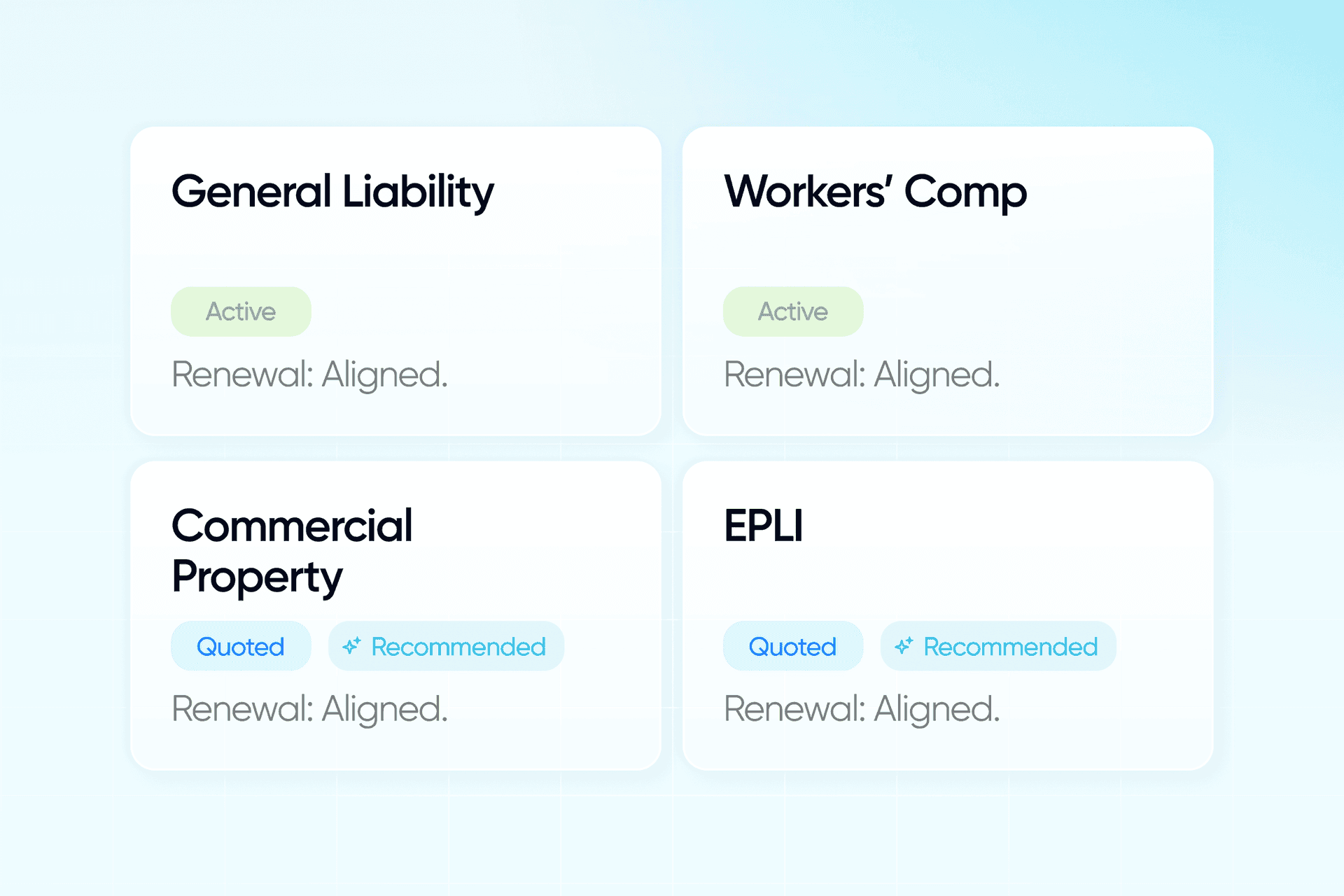

Most businesses that need a BOP also need workers’ comp.

If you have employees, workers’ compensation is typically required and should be coordinated with your liability and property coverage. Many businesses also need EPLI, cyber, or commercial auto depending on how they operate.

Infinite can quote your full stack together so limits align, renewals are simpler, and you can spot gaps across policies before they become expensive.

Why small businesses choose Infinite for BOP coverage.

Real reviews on fast comparisons, clear explanations, and support that makes renewals and certificates painless.

QUESTIONS & ANSWERS

FAQ

Have Questions? Talk to Us

By submitting, you agree to our Privacy Policy and Terms of Service.